Credit Repair for Buying a House

The Jones family just saved $32,300 on their mortgage repayments by improving their credit score before applying for finance.

See How Much You Could Save

Over 11% of US consumers are suffering from a poor FICO credit score. This figure is predicted to increase when the financial impact of COVID-19 hits harder in 2021. If you’re among this 11%, how can you buy a house with bad credit? Although you have less options, there are always routes to explore. Millions of Americans have a low credit score or no credit score at all and many are oblivious to their credit rating. A 2020 poll suggested that over half of US citizens have never checked their credit score at all, but it’s vital information when you apply for a home loan.

Credit Score to Buy a House

There is no credit score that guarantees you a loan or a mortgage since all lenders are free to set their own thresholds. The lower your credit score is, the less choice you have, and the more interest you are likely to pay.

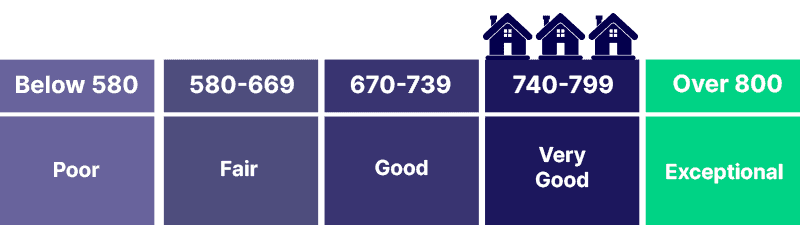

Below is a set of FICO score ranges that most lenders use;

- Below 580; a poor score that lenders will consider a risk.

- 580 to 669; a fair score that is below average but should be enough to secure a loan.

- 670 to 739; a good score that will satisfy most lenders as to your creditworthiness.

- 740 to 799; a very good score that proves you’re a responsible borrower.

- Over 800; an excellent score that denotes an exceptional borrower.

Over 90% of the leading lenders use FICO ratings as the basis for their lending decisions. The minimum credit score for home loans varies. Anyone hoping to keep their borrowing options open should aim for a “good” credit score of 670 plus. However, buying a house with bad credit is possible.

Home loan options

Let’s look at the choices you have with different credit scores:

- No credit score – VA loans officially require no minimum credit score and are for service or military personnel. A non-QM (non-qualified mortgage) may be possible for others.

- 300 to 500 – We advise you to raise your credit score first. But other options exist, such as a non-QM loan (as above).

- 500 to 579 – You are limited to an FHA home loan that requires a 10% down payment. These loans are backed by the Federal Housing Administration.

- 580 – 619 – You can get an FHA loan with a 3.5% down payment.

- 620+ – You can apply for a conventional home loan or mortgage adhering to Fannie Mae and Freddie Mac standards with a 3% down payment. These are the more popular mortgage types in the US. They are funded by private lenders such as banks, credit unions, and mortgage companies. USDA loans also fall within this bracket and offer benefits to buyers of rural homes.

How can I repair my credit before buying a house?

If you’re in one of the lower credit-score brackets listed above, you might be wondering how you can build up your credit score to buy a house. Well, there are several things you can do:

- Reduce credit card debt; pay off as much of your credit card debt as circumstances allow, if they allow it at all. Credit cards that are constantly maxed out harm your credit score.

- Improve payment history; begin paying bills on time and communicate with lenders if this is not possible to make other arrangements. Late payments stay on your records for at least seven years, but they harm your credit rating less and less over time.

- Use a credit repair service; this helps you check credit reports from the three major credit bureaus (Equifax, Experian, TransUnion) and dispute any false information. You can build your credit yourself (link to DIY tips to build your credit score) if the formalities don’t put you off.

- Rapid rescoring; some mortgage lenders can request an updated version of your credit score within five working days. Credit scores normally refresh each month, so a good recent repayment history makes a rapid rescore worthwhile.

- Take out a small loan and repay it; it helps to establish a recent history of repayment, but don’t take on a new loan you can’t afford. Be wary of applying for multiple credit accounts within a few weeks since a series of credit inquiries from lenders will hurt your score. You can gather loan quotes inside a 14-day period, because it counts as one inquiry.

Buying a house with bad credit

Bad credit home loans usually require a minimum credit score of 500. That’s the point where you qualify for an FHA loan if you can make a 10% down payment. Buying a house with bad credit often needs more capital in one form or another. Anyone struggling with a poor credit history can turn to the FHA for credit counseling and first-time-buyer advice.

Examples of US lenders that offer a low credit score mortgage include:

- Angel Oak Mortgage Solutions (sub-580 minimum)

- Athas Capital (sub-580 minimum)

- Carrington Mortgage Services (sub-580 minimum)

- CitiMortgage (580 minimum)

- Navy Federal Credit Union (580 minimum)

- New American Funding (580 minimum)

- PNC (580 minimum)

- Quicken Loans (580 minimum)

- Rocket Mortgage (580 minimum)

The minimum credit scores listed are for FHA loans. Other mortgage types usually need a 620 score or over. A credit score of 680 to 700 is average among American consumers. In 2020, the average credit score hit an all-time high of 711, and with financial help from the government they managed to keep it up. but it was buoyed by coronavirus assistance.

Can you buy a house with no credit?

Borrowers without a credit score or a sub-500 score can seek non-QM loans. These require the buyer to make a 20% to 35% down payment. A low score may need a higher down payment than no score, since the borrower is a proven risk. For the lender, a large down payment offsets risk because the borrower has a stake in the investment.

It takes at least six months to establish a FICO credit score, but a thin credit history is only slightly better than none. And living without debt does nothing to establish a credit history. Careful use of financial products improves a credit score, even if you have no need for loans and credit cards.

As you’d expect, buying a house with no credit history is hard. With fewer options, you are more likely to pay higher interest rates on the products you find. It’s vital to weigh up the long-term cost of your loan offers against other factors. Will your credit score improve soon? Or is your life about to change?

What is a good credit score for a first time home buyer?

First time home buyers are subject to the same credit score rules as everyone else. If they’re young and don’t have a great deal of money for a down payment, a credit score of 580 is desirable for an FHA loan. Anyone with a credit score of 680 or higher can apply for a conventional home loan, which may only need a small down payment and will have a lower interest rate.

Borrowers who can afford a 20% down payment avoid a monthly mortgage insurance premium. Insurance is one of the extra costs that buyers should weigh up. It’s not unusual for first-time buyers to ignore their credit score when applying for a mortgage. Here are some points to consider:

- Mortgage pre-approvals give first-time buyers an idea of what they can or can’t afford, based on their credit score. They are also seen as a positive sign of intent by lenders.

- Other major purchases on credit (e.g., a car) should be avoided just prior to applying for a mortgage. Lenders weigh up expendable income as well as credit history.

- Credit cards shouldn’t be maxed out. It’s best to stay within a third of utilized credit. Using nearly 100% of a credit limit is indicative of someone in hardship and/or without discipline.

- First-time buyers should remove inaccuracies from their credit files. You can dispute errors with the Credit reference agencies yourself or pay a credit repair company to fix the errors on your behalf.

- A first time home buyer may choose to wait and spend time improving their credit score. This will open the door to more attractive mortgage offers. Buying a house with bad credit is a last resort.

Common Questions

Can I get a low credit home loan to purchase a mobile home?

Not really, they are quite different. One main difference is that mobile homes are treated as personal possessions rather than homes unless the land they rest on is also owned. Thus, they are often funded with CHATTEL MORTGAGES rather than FHA loan of conventional mortgages. Chattel mortgages (or chattel loans) are usually repaid over a shorter period and at a higher interest rate.

Can I get mobile home financing with bad credit?

Yes. For example, the 21st Mortgage Corporation is a supplier of chattel mortgages in 46 US states. This lender welcomes borrowers with a sub-570 credit score, though they must have a 35% down payment in the form of cash, trade, or land equity

Do I need a minimum credit score to build a house?

If you want money to build your own home, you’ll typically need a construction loan. Lenders often seek a 680 to 70 credit score for this short-term loan, as it’s inherently riskier. However, there are companies (e.g., FMC Lending) that offer construction loan programs to applicants with bad credit. The down payment on a construction loan is usually 20 to 30% but equity-based deals are available.

Is Covid-19 going to impact the credit score needed to buy a house?

At the moment we are in uncertain times and it is hard to know how mortgage providers are going to react as a result of the coronavirus. It is likely that mortgage providers will only lend to those with a better credit score. Therefore, if you are thinking about buying a house in the near future, it is worth while to start repairing your credit today.