Credit Repair for Buying a Car

Karen just saved $9700 on her new Tesla car by improving her credit score before applying for finance.

See How Much You Could Save

After buying a house, buying a car might be the biggest purchase you’ll ever make. If you do not have all the cash at hand, you will have to borrow the money to fund your car purchase. When you apply to borrow money, the lender’s decision will be mostly based on your FICO credit score. If you have a bad credit score, it will probably be harder to be approved for a car loan. However, credit repair should fix your bad credit. In this article you will learn how to repair your credit before buying a car.

Buying a Car with Bad Credit

To buy a car with bad credit, you can apply for a loan from a bank or lender or you can approach a dealership directly. Before you decide which one you want to go with, there are things you should consider:

- The lower your credit score, the more you’ll pay in total for your car. One of the cruel ironies of bad credit is that it feeds off itself.

- The temptation when buying nice cars is to overestimate what you can afford to repay. You can’t rely on the lender to decide what is realistic for you.

- High interest means all the nice extras you’d like in a car effectively come at an inflated cost. Would you go to an expensive supermarket and fill up a trolley with overpriced groceries?

- Try getting a pre-approved loan from your bank, which lets you shop with confidence. If that fails, search for the best car dealerships for bad credit.

- Look for local non-profit agencies that may provide low-interest car loans to people and families with poor credit.

- Research online companies offering car loans for people with bad credit. Check their reputation and compare them, paying particular attention to interest rates.

- Get advice from a credible source before you begin your search for a car.

Bad credit car loans: dealers vs banks

Buying a car with bad credit through a dealership is fine, but you should tread carefully. Some dealers don’t have your best interests at heart. The louder they advertise bad credit financing, the more cautious you should be. Here are three ways dishonest car dealers may exploit bad credit customers:

- They’ll focus your attention on the affordability of monthly repayments rather than the large chunk of interest you’ll be paying off.

- Desperate buyers offer the path of least resistance to salesmen because their leverage for negotiating price and any extras is close to zero.

- Unscrupulous dealers may charge you interest at a higher rate than the one quoted by the underlying lender and then pocket the difference.

before visiting a dealership. For instance, borrowers with very low 300-500 FICO credit scores can expect to pay an average interest rate of 20.67% for a secondhand car (source: Experian). You can find out what your credit score is from the myFICO website or its partners and research the ballpark interest rate you should be paying based on that. To offset the high-interest rates payable on low-credit car loans, it’s a good idea to make the biggest down payment you can. With banks, you can be confident that the loan they propose is their best offer. But you still need to shop around for the lowest interest rates and most attractive terms.

Car dealerships that work with bad credit

If you fancy keeping things simple, you can skip bank loan applications and head directly to the car dealership. There may be several car dealerships that work with bad credit near you, but they’re not all the same. There are three basic types:

- Franchise dealerships sell cars of one brand, either new or almost new. Of course, that means the cost is likely to be higher. Car manufacturers like Ford, BMW, Honda, Nissan, and others run their own finance companies. You might visit these places if your credit score is a little below average, but you’ll usually need a credit score in the 600s. One benefit of these establishments is the high value they place on reputation.

- Traditional independent dealerships usually work with an array of banks and financial institutions, so it’s worth seeing what they have to offer. But don’t be pressured into buying a car on the spot. These dealerships will sell cars of all ages and types. Traditional dealers are a good idea if you want an independent lender without having to sort the details out yourself. One downside is that you empower the dealer and not yourself. But dealers are highly motivated to find you a solution.

- Buy Here, Pay Here (BHPH) car lots provide all their financing in-house rather than going through a third party. These dealerships specialize in supplying cars to people with bad credit. Be a little wary of them, because they have a reputation for deception. Some are good and some are bad, so you must do your homework before visiting. Always check the true value of the car you intend to buy to make sure the

loan isn’t being inflated.

Credit score for car loan

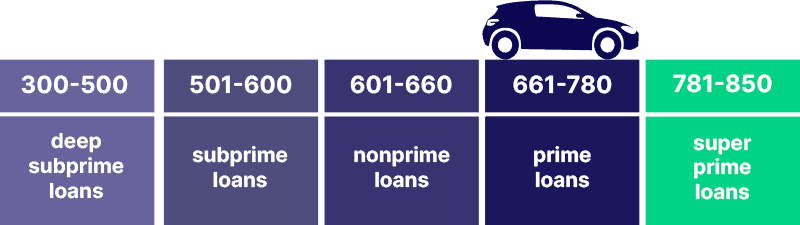

Credit scores for the purpose of buying a car aren’t much different from those for a home loan or any loan. Car loans fall into these brackets, based on the FICO credit score:

- 300-500 – deep subprime loans for borrowers with a very low credit score. These loans have high interest rates (average around 20% for used cars.)

- 501-600 – subprime loans for people with bad credit, where the interest rates are just a few percent below deep subprime.

- 601-660 – nonprime loans for credit scores a little below average. Interest rates may be half those of a deep subprime loan.

- 661-780 – prime loans for consumers with an average or above-average credit score. At this point, average interest rates are a third of deep subprime.

- 781-850 – super-prime loans for those with exceptional credit scores. Here, the average interest rate is up to five times lower than bad credit car loans.

As you can see, there’s a vast difference between the amount of interest you pay with bad and good credit. That’s why it’s always recommended to raise your credit score first, if you can, rather than going for bad credit finance. Don’t buy a car with bad credit unless you have an urgent need of one and/or can’t change your situation.

Repair your credit score for a bigger choice of cars

FICO credit scores are generally updated each month. Therefore, you can work on improving a bad credit score in the months leading up to a car purchase. Here are three things to do:

- Make sure you pay all your bills on time or make alternative payment arrangements if that is not possible. Communication with lenders is vital if you’re in hardship.

- Get the balance on credit cards down to a third or less of the maximum. If you never have any spare credit, it hurts your credit score.

- Repair your credit yourself by ordering a credit report and applying to have any errors removed. If you find the formalities of doing this stressful or too time consuming, you can have a credit repair company do the work for you.

Credit score to lease a car

Leasing a car is like long-term car hire. You pay a sum of money each month to drive a decent car around, and maintenance is usually included in the cost. At the end of the term, you give the car back, or you may have the chance to buy it for a lump sum. So, what credit score do you need to lease a car?

As with regular car loans, you’ll get better deals if you have a credit score of at least 600 and preferably nearer 700. But you can also lease cars with a credit score of 500. The downside is, you’ll pay a higher monthly rate and may have to make a big down payment.

You can improve your chances of leasing a car if you can find a co-signer with good credit willing to guarantee your repayments. But that can destroy relationships if it goes wrong!

Used cars & bad credit

One thing to note about buying used cars on bad credit is the interest rate on loans is often higher. Why? Because second-hand cars depreciate unpredictably. If the lender must repossess the car and it’s worth nothing, it makes a loss. Higher interest rates offset that risk.

The plus side of buying a used car is that it’s easier to stay within your financial limits. As well, the 10-20% down payment that may be necessary with poor credit is more doable if the price of the car is only a few thousand dollars.

Common Questions

How do I find dealership that work with bad credit?

Most dealership work with bad credit to some degree, though the big franchise dealers are less likely to help unless you have a thin credit history (i.e. you haven’t borrowed much money). Visit more than one dealer to compare prices and check the value of car you’re looking at online.

What’s a good credit score to buy a car?

Most dealership work with bad credit to some degree, though the big franchise dealers are less likely to help unless you have a thin credit history (i.e. you haven’t borrowed much money). Visit more than one dealer to compare prices and check the value of car you’re looking at online.

What can I expect from bad credit – no credit dealerships?

Dealerships that specialize in bad credit are the “Buy Here, Pay Here” variety. These can offer you a loan under most circumstances because they don’t rely on a third party for approval. However, you should make sure this level of control isn’t being abused.

Is buying a car with no credit possible?

Yes. Bad credit specialists pay little attention to your credit score, but they may want a large down payment. You can also achieve this by getting a cosigner to act as a guarantor for repayments.

Is there such a thing as car loans with bad credit & no money down?

The ability to make a down payment makes you more appealing to lenders, but you can find bad credit loans that need no money down. You’ll probably need proof of steady income and a long-term address.