Credit Repair for Loan Approval

Matt repaired his credit and secured a low interest loan after using Renoix for 4 months.

See How Much You Could Save

Most of us take out a loan at one time or another, whether for a vacation, a new kitchen, a fancy new camera or TV, or even for paying off other loans. However, getting approved for a loan isn’t so easy if your credit score has taken a dive or you have no credit history. In this article, you’ll learn how to build and repair your credit score to be approved for a loan!

How to Get a Loan with No Credit

Most banks and financial institutions use the FICO credit score to make lending decisions. But there are vast numbers of US residents who don’t have a credit score. Here are four possible reasons why you might not have one:

- You are young and have never borrowed money.

- You haven’t been named on any utility bills (e.g. if you are a lodger).

- If you haven’t applied for credit in many years. Positive credit history vanishes after 10 years, whereas negative history takes seven years to disappear.

- You’ve recently moved to the US from another country.

Loan companies like to see that you’re trustworthy before lending you money; no surprise there. Theoretically, you can have a high-paid job and still have no credit score. This leads to the inevitable question; can I get a loan with no credit? The answer is yes. However, will you want to apply for a loan with no credit history or a very bad credit loan, you’ll probably be paying higher interest on the loans you can get.

So, are you in a hurry for the money, or do you have time to build a credit score over a few months? You don’t need loans to build your credit score. Simple actions such as putting utility bills in your name and paying for your cell phone usage (i.e. a postpaid plan) can build your credit score.

Other ways to prove you are low risk for a loan with no credit history

Loans for people with no credit are more likely granted when applicants prove they’re low risk. You can do this in several ways:

- Get a full-time, secure job with a steady income. Irregular income may make lenders nervous.

- Demonstrate that you have enough expendable income to make loan repayments comfortably. This is the difference between your monthly earnings and outgoings.

- Show bank invoices with regular savings.

- Make sure any bills you take on which are in your name are promptly repaid. It only takes a month for credit history to refresh, even though it will be thin at that point.

Getting a bad credit loan online

Personal loans for bad credit can be more challenging to obtain than a loan with no credit. At least, they are if you want a lower rate of interest. Once you have a bad credit score, you’re a proven risk rather than an unknown one.

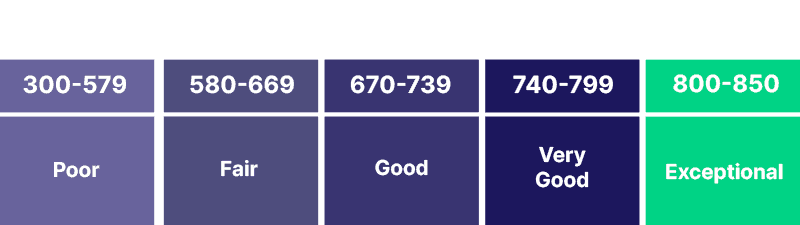

When you apply for a loan with no credit score, you may be able to prove you’re not a risk. That possibility doesn’t exist when you apply for a loan with poor credit. So, if you want to borrow money with decent interest rates, you must increase your FICO credit score. In the context of a personal loan, FICO scores break down as follows:

- 300 to 579; poor

- 580 to 669; fair

- 670 to 739; good

- 740 to 799; very good

- 800 to 850; exceptional

(Source: Experian)

According to Experian, 16% of US consumers in 2020 fall into the first bracket and have a poor credit score. Together with those who have no credit score, that accounts for tens of millions of people.

How to repair your credit to increase your chances of loan approval

Don’t want to get a payday loan for bad credit because of the high-interest rates? If you know you’ll need to apply for credit in the future and you want to increase your loan options, you can work on improving your credit score in the interim. There are multiple ways to go about this:

- Make sure all bills in your name are paid on time and communicate with creditors if this is not possible to set up an alternative schedule. Late payments stay on your history for seven years, but they fade in gravity over time.

- Get any credit card balances down to 30% of credit utilization or lower. Using a credit card is beneficial, but maxed-out credit hurts your FICO score.

- Repair your credit score either using a credit repair company or by ordering your reports and meticulously chasing down errors. You begin this process by applying for credit histories from TransUnion, Equifax, and Experian.

- Avoid applying for numerous other loans or forms of credit before your main personal loan. Multiple inquiries on your credit history for credit applications hurt your score unless they’re within a short space of time (14 days) for gathering quotes.

- Look at other ways to enhance your credit score, such as using the free Experian Boost service. This ensures your credit goes up by paying for bills, cell phone plans, and streaming services.

- Become an authorized user on someone else’s account with a good credit score.

- Don’t close unused credit cards because their zero balance will be factored into your credit utilization ratio.

Some of these tips will also help you get a loan with no credit, too, over time. I.e. getting your name onto utility bills and linking yourself to creditworthy people. Building and repairing a credit score both take time, but the efforts pay off.

No Credit Check Loans

Online loans with no credit check seem attractive at first glance since lenders make an instant decision and tempt you by offering money straight away. However, many of them come with a hideous interest rate of between 100% to 1000% APR and over. That means your repayments will go mostly towards interest while the actual balance barely moves. Payday loans with no credit check are not recommended, especially when the repayment term is long.

Getting an Emergency Loan for Bad Credit

There are times when same day loans for bad credit are your only option. A prime example of this is if you are suddenly faced with medical bills that you can’t afford. Some lenders specialize in providing emergency cash immediately with bad credit. Although they still charge relatively high interest at over 25% APR, this is much better than facing the exorbitant interest rates of no credit check loans.

One thing to check when taking out high-interest emergency loans for bad credit is whether there is a penalty for early resettlement. By making larger repayments and ending the loan early, you can significantly reduce the total cost of borrowing. But some lenders will charge you a fee for the privilege.

Common Questions

Should I consider secured loans for bad credit?

You can use any assets you possess as collateral to get a loan for bad credit. It could be a house, car, stocks, or bonds. Secured personal loans for bad credit are often a better option than a no credit check loan because the interest rates are lower, but you do stand to lose the collateral if you don’t make repayments. Ultimately, unsecured loans are better if the terms are no scandalous.

What are my chances of getting a 550 credit score loan?

A 550 credit score isn’t as bad as FICO scores get, but you’ll struggle to get a loan from any popular bank with it. Banks usually prefer a good credit score in the upper 600s. In general, you’ll be looking at higher interest rates from specialist lenders. Let’s say you took out a loan for $2000 over two years with a high-interest rate of 35% APR. You’d end up paying $808 in interest: over $650 more than you’d pay with good credit.

What are the best banks for bad credit

Although many banks are reluctant to loan money to people with bad credit, some of them will help you to get back on your feet by letting you open a “second chance account.” In doing this, they disregard any negative aspects of a ChexSystems Report on your banking history. You can take advantage of facilities such as online bill pay to get organized and improve your FICO score.

Can I get a credit union loan for bad credit?

Credit unions are not-for-profit organizations that you usually pay a fee to join, provided you meet their criteria. You can join a credit union with bad credit, and they may be able to offer you a loan at a lower interest rate than bad-credit specialists.Add block